💰 US Federal Reserve Rate Cut 2025: Will Home, Bike, and Personal Loans Get Cheaper?

On September 17, 2025, the US Federal Reserve (Fed) announced its first interest rate cut of the year, reducing the federal funds rate by 25 basis points (0.25%). The new target range now stands at 4.00% – 4.25%.

The move has sparked an important question for millions of Americans: Will this make loans—like home mortgages, bike/car loans, personal loans, and even credit cards—cheaper?

Let’s break it down in detail.

🏦 What Exactly Did the Fed Do?

- The Federal Open Market Committee (FOMC) voted to cut rates by 0.25%.

- Fed Chair Jerome Powell announced the decision, citing a slowing labor market, weaker GDP growth, and easing inflation pressures.

- This is the first cut in 2025, after nearly a year of holding interest rates steady at a two-decade high.

- Governor Stephen I. Miran dissented, pushing for a deeper cut of 0.50%, but the majority chose a cautious 0.25%.

The Fed’s goal: support growth and jobs without reigniting high inflation.

📉 Why Does the Fed Rate Matter for Loans?

Most loans in the US are tied—directly or indirectly—to the Fed funds rate or the prime rate (which is about 3% higher than the Fed funds rate).

When the Fed cuts rates:

- Prime rate falls → banks pass on cheaper borrowing costs to customers.

- Bond yields fall → mortgage and auto loan rates may dip.

- Credit card APRs—linked to prime—also go down.

In short: borrowing gets cheaper. But how fast and how much depends on the loan type.

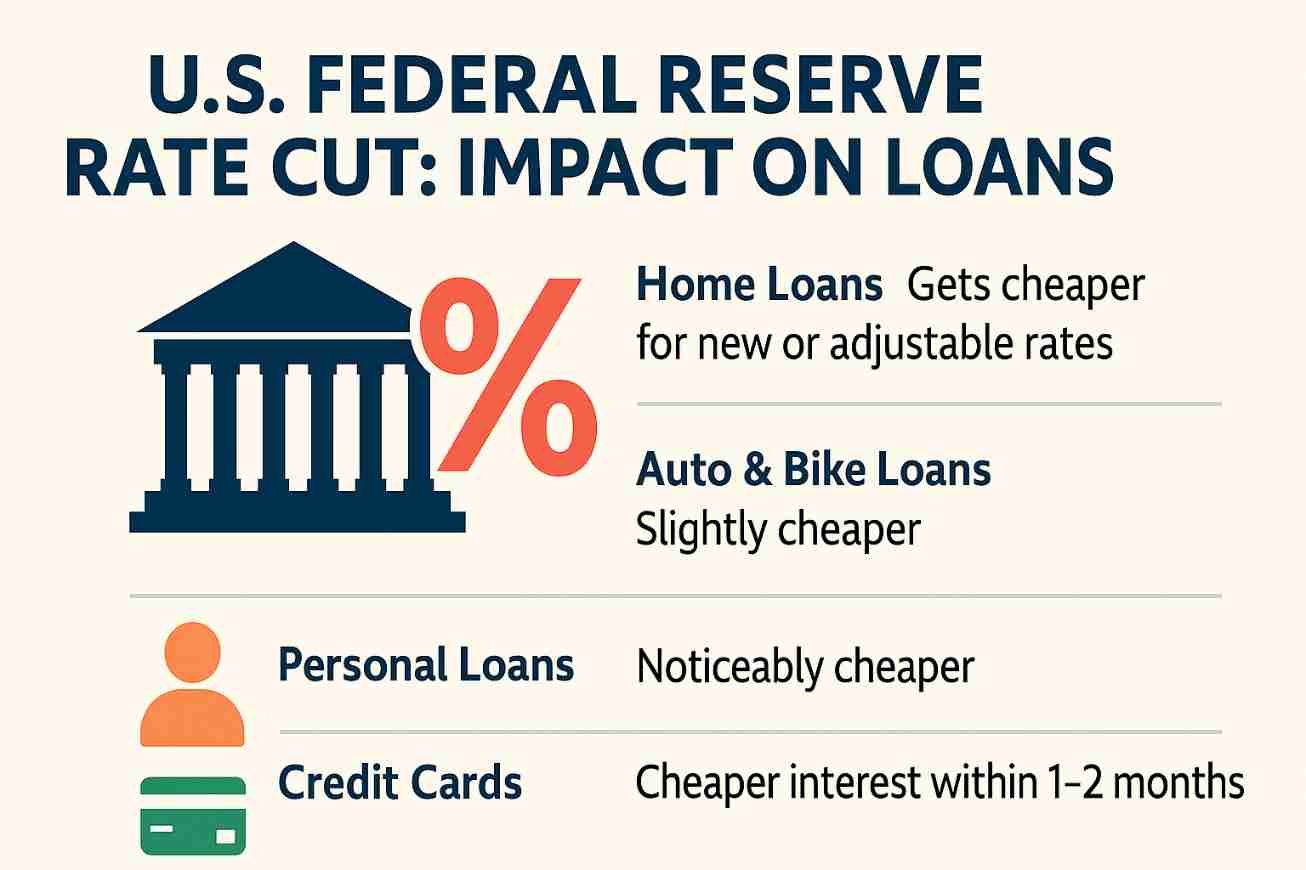

🏡 Home Loans (Mortgages)

- Fixed-rate mortgages:

- If you already locked a fixed rate, nothing changes.

- But new borrowers could see slightly lower 30-year or 15-year mortgage rates, depending on Treasury bond yields.

- Adjustable-rate mortgages (ARMs):

- These adjust periodically and are closely tied to Fed rate changes.

- Expect ARMs to get cheaper within months.

📊 Impact: New mortgage seekers may benefit; existing fixed-rate homeowners won’t unless they refinance.

🏍️ Auto & Bike Loans

- Auto/bike loans are based on the prime rate + lender’s margin.

- With the prime rate falling after the Fed cut, new car or bike loans should become slightly cheaper.

- Example: If an auto loan was offered at 7.5%, it could drop to around 7.25–7.3%, depending on credit score and lender.

📊 Impact: Small but noticeable relief for buyers planning big-ticket purchases.

👤 Personal Loans

- Personal loans are usually unsecured and have higher interest rates.

- They are directly tied to the prime rate.

- When the Fed cuts rates, banks immediately adjust personal loan rates downward.

📊 Impact: Personal loans are among the first to get cheaper, making debt consolidation and emergency borrowing less costly.

💳 Credit Cards

- Most US credit cards have variable APRs linked to the prime rate.

- With the Fed’s 0.25% cut, APRs will also drop by 0.25%.

- The change typically shows up in your bill within one or two billing cycles.

📊 Impact: High-interest debt on credit cards will become slightly less expensive, though rates remain high overall (20%+ APR for many cards).

📊 At a Glance: Which Loans Get Cheaper?

| Loan Type | Effect After Fed Cut 🟢 |

|---|---|

| 🏡 Fixed-rate mortgage | ❌ No change (only new borrowers benefit) |

| 🏡 Adjustable-rate mortgage | ✅ Gets cheaper soon |

| 🏍️ Auto/Bike loans | ✅ Slightly cheaper |

| 👤 Personal loans | ✅ Noticeably cheaper |

| 💳 Credit cards | ✅ Cheaper within 1–2 billing cycles |

🇺🇸 Impact on the US Economy

The Fed hopes the cut will:

- Boost consumer spending by making borrowing easier.

- Encourage business investment through cheaper financing.

- Prevent a rise in unemployment by supporting demand.

But risks remain:

- If inflation rises again, the Fed may have to pause or reverse course.

- Too many cuts too fast could weaken the dollar and push up import prices.

🌏 Global and Indian Context

The Fed’s decision also has ripple effects worldwide:

- For India:

- Foreign Portfolio Investment (FPI) inflows may increase.

- The rupee could strengthen against the dollar.

- Imports like oil and gold may become cheaper, though exporters might feel pressure.

- For the World:

- Emerging markets benefit from cheaper capital.

- Dollar weakness may push commodity prices (oil, gold, metals) higher.

- Currencies like the euro and yen may strengthen, impacting European and Japanese exporters.

🔮 What’s Next?

- The Fed has hinted at two more cuts in 2025, depending on economic data.

- If unemployment continues to rise and inflation stays under control, more easing is likely.

- But if inflation unexpectedly jumps, the Fed may hit pause.

✅ Key Takeaways

- The Fed cut rates by 0.25% in September 2025.

- Personal loans, bike/auto loans, and credit cards will become cheaper the fastest.

- Home loans benefit mostly for new or adjustable-rate borrowers.

- For the US, this is a balancing act: support jobs while keeping inflation in check.

- Globally, the cut influences currencies, trade, and capital flows.

📌 Conclusion

The US Federal Reserve’s September 2025 rate cut is small but significant. It signals a shift in policy after years of focusing on inflation. For everyday Americans, the biggest relief will come in the form of cheaper personal loans, credit cards, and vehicle loans. Mortgage relief will take longer, and only adjustable or new borrowers will feel the difference quickly.

Globally, the move reshapes trade, capital flows, and commodity markets. For India and other emerging economies, the cut opens opportunities for growth but also brings new challenges for exporters.

In short: What happens in Washington doesn’t stay in Washington — it affects your wallet, whether you’re in New York, Mumbai, or Tokyo.

❓ Frequently Asked Questions (FAQs) on Fed Rate Cut 2025

1. What exactly did the US Federal Reserve cut in September 2025?

The Federal Reserve reduced the federal funds rate by 0.25% (25 basis points), bringing the target range down to 4.00%–4.25%. This is the interest rate banks charge each other for overnight loans and it influences borrowing costs across the economy.

2. Does this mean all loans in the US are now cheaper?

Not immediately. Personal loans, credit cards, and auto/bike loans linked to the prime rate will become cheaper within weeks. Adjustable-rate mortgages also fall soon. But fixed-rate mortgages remain unchanged unless you refinance.

3. Will my home loan EMI go down after this Fed cut?

- If you have a fixed-rate mortgage, your EMI will not change.

- If you have an adjustable-rate mortgage (ARM), your payments will likely reduce when your rate resets.

- New home loan applicants may get slightly lower interest rates.

4. Are personal loans and credit cards affected quickly?

Yes ✅. Since these are linked directly to the prime rate, interest charges drop by the same margin (0.25%) usually within one or two billing cycles.

5. How much cheaper will bike or auto loans become?

The reduction is small but noticeable. For example, if your car loan was at 7.5%, it may now drop to around 7.25%–7.3%. The exact change depends on your credit score and lender.

6. Why did the Fed cut rates now?

The Fed acted because:

- US job growth has slowed.

- GDP growth is moderating.

- Inflation is easing toward the 2% target.

The cut is meant to support the economy and prevent unemployment from rising too fast.

7. Will there be more Fed rate cuts in 2025?

Yes, the Fed has signaled that two more rate cuts may come later in 2025, depending on economic data like jobs, inflation, and global risks.

8. How does this affect India?

- More foreign investment inflows may come to Indian markets.

- The rupee may strengthen against the dollar.

- Imports like oil and gold may become cheaper.

- Exporters may face pressure if the dollar weakens too much.

9. Does a Fed rate cut always mean good news?

Not always. While borrowing becomes cheaper, there are risks:

- Inflation could rise if demand spikes.

- The dollar could weaken, making imports expensive.

- Too many cuts could signal that the US economy is in deeper trouble than expected.

10. What should US borrowers do after this rate cut?

- Credit card holders: Expect lower APRs soon, but continue paying off high-interest debt quickly.

- Homeowners with ARMs: Watch for lower payments on your next reset.

- New borrowers: This could be a good time to shop for mortgages, personal loans, or auto loans.

Here are the effects of the US Fed rate cut on the Indian stock market, based on recent reports and expert analysis:

📈 What’s happening in Indian Markets after the Fed Cut

- Markets opened higher

After the Fed cut rates by 25 bps, Indian indices like Sensex and Nifty-50 opened higher.- Nifty50 rose ~0.44%

- Sensex gained over 300 points on optimism following the Fed action.

- IT & Banking sectors leading the gains

- IT stocks are benefiting especially, given their revenue exposure to the US market. Lower US rates make demand and client budgets more favorable.

- Banking & financials may also see positive reaction due to cheaper global funding and capital flows.

- Foreign Institutional Investor (FII) flows may improve

- Lower US yields make Indian equities more attractive. Experts believe FPIs may return more actively.

- This can add liquidity and upward momentum to Indian stock indices.

- Rupee strengthens modestly

- The rupee saw some appreciation or strengthening following the cut, partly due to a drop in the US dollar.

- A stronger rupee helps reduce cost of imports and may improve margins for companies dependent on imported inputs.

⚠️ Caveats & Limited Effects

- Much of the Fed cut was already priced in by the markets. So the immediate effect is modest.

- The impact tends to be more for sectors sensitive to global demand & exporters, while more domestic‐focused sectors may see less effect.

- Macro factors in India (inflation, policy changes, RBI actions, global trade environment) still matter a lot — the Fed cut is just one of the influences.

“Disclaimer: This content is informational only, not financial advice.”